Insurance Claim Deadline vs. Lawsuit Deadline: Two Timelines People Mix Up

Insurance Claim Deadline vs. Lawsuit Deadline: Two Timelines People Mix Up

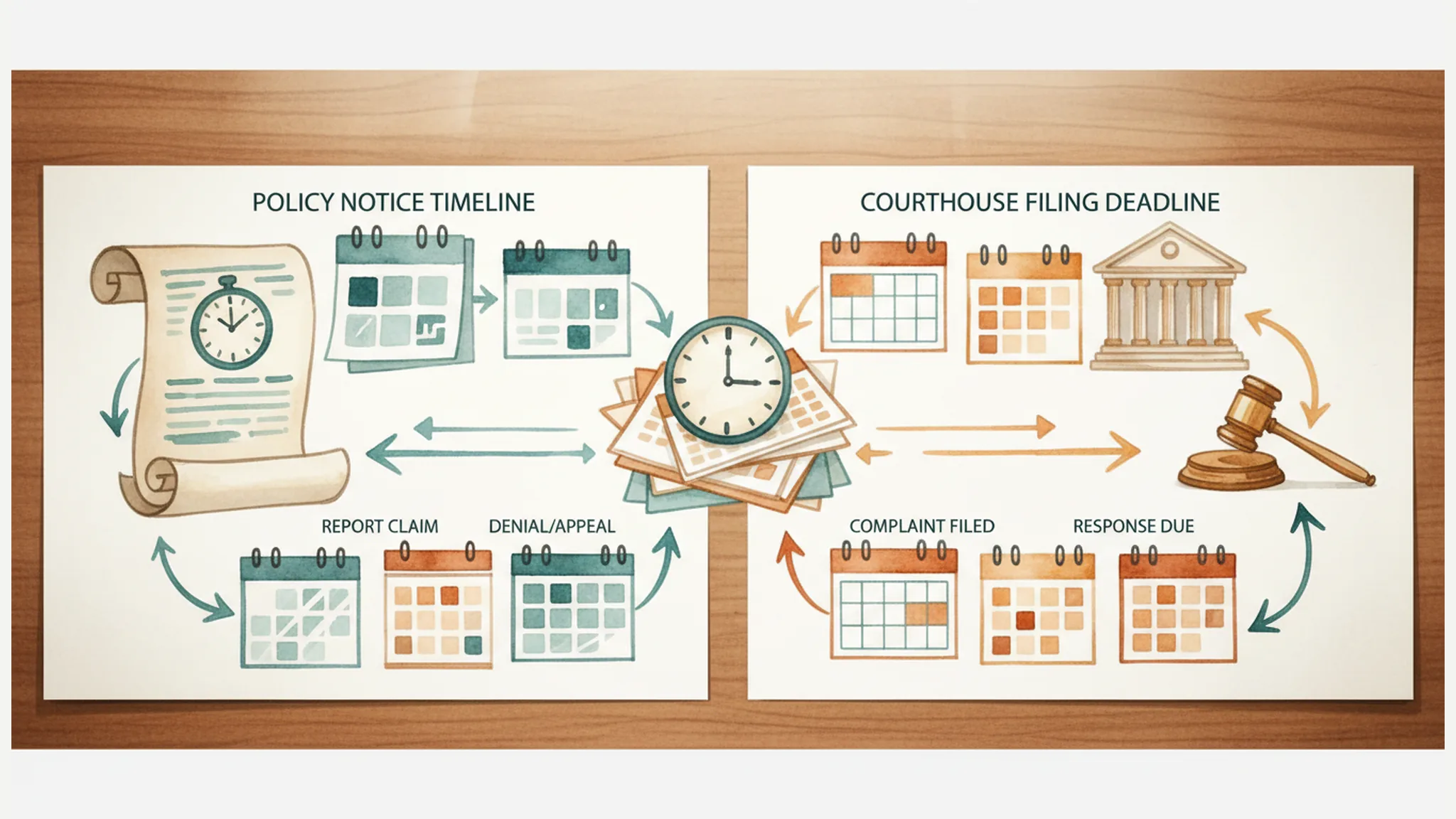

After an Oregon crash or injury, people often ask one deadline question: “How long do I have?” The safer answer is usually: which deadline are we talking about?

An insurance claim deadline is not always the same thing as a lawsuit deadline. Policy notice duties, proof-of-loss requirements, PIP or UM/UIM conditions, government tort-claim notice, and the statute of limitations can all point to different dates. Settlement talks do not automatically make those dates disappear.

This article is educational information only, not legal advice. Do not use it to calculate the last day to act. Deadline analysis is fact-specific and should be checked early.

The Simple Difference

An insurance claim deadline usually comes from an insurance policy, claim-handling rule, benefit statute, or insurer request. It can involve reporting the loss, cooperating with the investigation, submitting forms, providing proof of loss, or preserving a right to benefits.

A lawsuit deadline is the deadline to start a court case. In many Oregon personal injury claims, ORS 12.110 provides a two-year period for injuries to the person or rights of another, unless a more specific rule applies. Some cases have different rules, exceptions, shorter notice requirements, or separate statutes.

Do not assume that meeting one timeline satisfies the other. Reporting a claim to insurance is not the same as filing a lawsuit. Filing a lawsuit is not the same as satisfying every policy condition.

Oregon Claim-Handling Timelines Are Not Your Only Deadlines

Oregon claim-handling rules require insurers to respond and investigate within certain timeframes. Those rules matter, especially when the insurer delays. For example, insurers generally must acknowledge receipt of a claim notice or pay within 30 days, reply within 30 days to pertinent claim communications that reasonably call for a response, and complete investigations within 45 days unless more time is reasonably needed.

Those are insurer conduct rules. They are not a substitute for your own legal deadlines. An adjuster can be communicating with you while a statute of limitations, public-body notice period, or policy deadline is still running.

If the insurer is using delay tactics, see Delay, Deny, Defend and keep a written timeline.

Public-Body Claims Can Have a Much Shorter Notice Deadline

If a city, county, state agency, public transit provider, school district, or public employee may be involved, Oregon Tort Claims Act notice can become urgent. ORS 30.275 generally requires notice within 180 days for non-wrongful-death claims against public bodies, with specific rules for formal notice, actual notice, and exceptions.

That 180-day notice issue is different from the general two-year lawsuit period. Missing the notice requirement can create serious problems even when the two-year period has not expired. Claims involving public vehicles, road design, work zones, sidewalks, transit, or government property should be screened early.

PIP, UM/UIM, and Policy Duties Can Add More Timelines

Oregon private-passenger auto policies generally include personal injury protection benefits for specified people, including insureds, passengers, and pedestrians struck by the insured vehicle. PIP benefits can involve proof-of-loss and benefit procedures. UM/UIM claims may involve separate policy conditions, notice duties, consent issues, or arbitration language.

The important point is not to memorize every possible insurance condition. The important point is to ask early:

- What policies may apply?

- Who needs notice?

- What forms or proof are required?

- Is there a deadline in the policy?

- Is a public body involved?

- Is a lawsuit deadline separate from the claim deadline?

Settlement Talks Do Not Automatically Pause the Lawsuit Clock

Insurance negotiations can make a claim feel active. That does not necessarily mean the lawsuit deadline is paused. If an adjuster is discussing settlement, requesting records, or making offers close to a deadline, get clarity before assuming negotiations protect you.

Oregon rules restrict certain insurer statements near time limits. For example, in some direct negotiations with an unrepresented claimant, Oregon rules may require written notice before a statute of limitations or policy time limit the insurer believes may affect the claimant’s rights. But relying on the insurer to warn you is risky. Track deadlines yourself.

This is especially important when the insurer makes a quick settlement offer or says it is waiting on documents while the calendar keeps moving.

A Practical Deadline Checklist

As soon as possible after a crash or injury, write down:

- Date and location of the incident.

- Every potentially responsible person or entity.

- Whether any public body, public employee, transit agency, school, city, county, or state agency may be involved.

- All insurance policies that may apply: your auto policy, household policies, the other driver’s policy, employer or commercial policies, PIP, UM/UIM, health insurance, or premises coverage.

- Date each insurer received notice.

- Any written deadline, proof-of-loss request, examination request, or form request.

- Any denial, partial denial, or reservation of rights.

- The likely lawsuit deadline, checked against the specific claim type.

For communications, save your own record and compare it with the insurer’s requests. The companion posts on claim-file notes and what to save after adjuster calls can help.

Sources

- ORS 12.110, Actions for certain injuries to person

- ORS 30.275, Oregon Tort Claims Act notice

- ORS 742.520, Personal injury protection benefits

- OAR 836-080-0225, Required Claim Communication Practices

- OAR 836-080-0230, Standard for Prompt Claim Investigation

- OAR 836-080-0235, Standards for Prompt and Fair Settlements

Client-First Fee Promise

Client First = Bills First, Fees Second

Your unpaid medical bills do not have to make your lawyer's fee bigger. Johnson Law subtracts qualifying medical bills before calculating our fee, helping clients keep more of their settlement.

Applies to qualifying cases. Results vary.