Motorcycle Totaled, Gear Destroyed: Can You Recover Helmet/Jacket/Aftermarket Parts Value?

Motorcycle Totaled, Gear Destroyed: Can You Recover Helmet/Jacket/Aftermarket Parts Value?

Educational information only, not legal advice. Oregon motorcycle property and insurance issues are policy-specific and fact-specific. This article explains common claim rules and documentation problems after a serious crash.

After a serious motorcycle collision, riders often focus on the bike first.

That makes sense. A totaled motorcycle is hard to ignore.

But another part of the loss is often under-documented at the worst possible time:

- helmet,

- jacket,

- gloves,

- boots,

- luggage,

- phone or camera mounts,

- hard bags,

- and aftermarket parts or accessories on the bike.

Those losses may matter for money, but they also matter for proof. A torn jacket, crushed helmet, broken saddlebag mount, or scraped fairing can help show how the crash happened and how the rider’s body took the force.

If you want the broader injury-side context first, see our motorcycle accident practice area page, our article on preserving evidence after an accident, our post on motorcycle rear-end injuries at a stop, and our Oregon guide to motorcycle UM/UIM claims after severe injuries.

1) Quick answer

Often, yes.

After an Oregon motorcycle crash, a rider may be able to pursue payment for destroyed riding gear and some aftermarket parts. But the answer depends on several different questions:

- Who is paying? The at-fault driver’s insurer, your own carrier, or both at different stages?

- What exactly was damaged? The motorcycle itself, attached accessories, or separate personal property?

- What proof do you have? Receipts, pre-crash photos, install records, model information, and damage photos all matter.

- What does the policy actually cover? First-party coverage for gear and custom parts is not automatic just because the bike is insured.

2) Why this is not “just” a property-damage issue

Oregon defines economic damages broadly enough to include reasonable costs due to loss of use of property and reasonable costs for repair or replacement of damaged property. See ORS 31.705.

For motorcycle cases, that matters in a practical way.

Destroyed gear and accessories are often part of the overall crash loss, not a separate sideshow. The same helmet or jacket that may support reimbursement can also support the bodily-injury claim by showing:

- where impact occurred,

- whether the rider slid,

- whether the head or shoulder took force,

- whether a leg or foot got trapped,

- and whether the crash mechanics fit the medical record.

That is one reason riders should be very careful before throwing anything away.

3) The first distinction is who is paying the claim

This is where people get confused fast.

The at-fault driver’s liability claim

If another driver caused the crash, damaged riding gear and some bike-related property may be part of the liability claim along with bodily injury.

But Oregon minimum liability limits are not large. Under ORS 806.070, minimum limits generally include $20,000 in property damage.

In a serious motorcycle crash, that property-damage limit can be consumed by:

- the bike itself,

- towing and storage issues,

- damaged accessories,

- and riding gear or other crash-damaged items.

Your own first-party claim

If you use your own coverage, the claim becomes more policy-specific.

That may involve:

- collision or comprehensive for the bike,

- accessory or custom-parts coverage if purchased,

- appraisal language in the policy,

- deductibles,

- and subrogation later if another driver was actually at fault.

Under ORS 742.466, Oregon addresses appraisal-style resolution of certain physical-damage disputes under motor vehicle policies.

Do not assume every personal item is covered by motorcycle insurance

Oregon DFR’s auto-insurance FAQ says auto policies generally do not cover personal property stolen from a vehicle or damaged in an accident.

The safest motorcycle-specific takeaway is narrower: do not assume your own motorcycle policy automatically covers every non-bike item that was damaged just because it was on or with the bike. Check the actual policy.

4) The bike’s value, the gear’s value, and the aftermarket parts value may all be treated differently

One of the biggest claim traps is treating everything as one big number.

It usually is not.

The motorcycle’s pre-loss value

When an insurer declares the motorcycle a total loss, the bike itself is usually valued as a pre-loss vehicle, not by emotional attachment and not by the current loan balance.

Oregon DFR explains that the owner is generally owed what the vehicle would have been able to sell for before the accident and that insurers typically use valuation services to determine that amount.

Attached aftermarket parts and accessories

This is where many riders get frustrated.

The fact that you spent money on an exhaust, bags, crash bars, lighting, seat, or other custom parts does not automatically mean the insurer adds that full invoice amount to the total-loss payment.

The real argument is usually about supported pre-loss value:

- Was the part actually installed?

- Was it visible in pre-crash photos?

- Is there a receipt or service invoice?

- Did it add market value to this bike?

- Was it subject to a custom-parts or accessories limit under the policy?

Separate damaged gear and personal property

Helmet, jacket, gloves, boots, luggage, and similar items may need their own proof.

That is especially true if the insurer tries to treat them as separate personal property rather than part of the bike valuation.

5) Oregon total-loss rules give riders some useful valuation rights

If an insurer declares a motorcycle a total loss and offers a cash settlement, Oregon law provides some important disclosure and dispute-process protections.

You should get the valuation material

Under ORS 742.554, the insurer must provide any valuation or appraisal reports relied on to determine value, along with the required written total-loss statement.

That matters because riders should not just react to the number. They should review the underlying assumptions:

- correct year, make, and model,

- mileage,

- equipment and options,

- condition adjustments,

- and whether comparable vehicles are actually comparable.

Oregon DFR likewise tells consumers to review the valuation carefully and correct differences in miles, equipment, condition, and comparable vehicles.

Undisputed amounts may still have to be paid

Under ORS 742.558, if the insurer and owner cannot agree on value, the insurer generally must pay the amount not in dispute once the statutory conditions are met for transfer and inspection.

That does not settle the disagreement forever. It just means a valuation dispute does not always justify holding everything back.

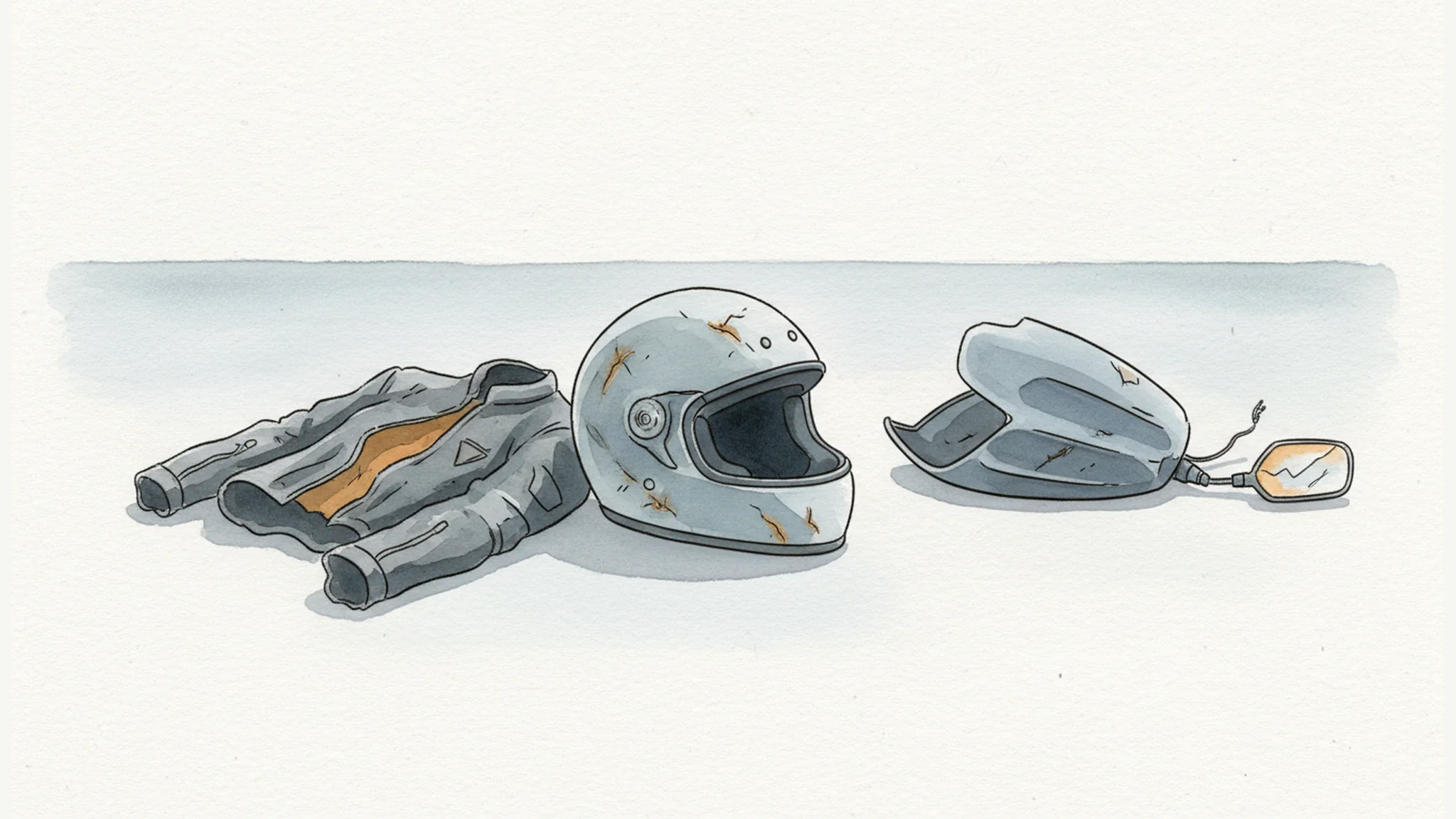

6) Why you should preserve the helmet and gear even if they look ruined

Riders sometimes assume a destroyed helmet or jacket is just trash after the crash.

That can be a mistake.

Damaged gear may help with:

- proving a property-loss amount,

- showing contact points,

- supporting the mechanism of injury,

- and countering insurer arguments that the crash was too minor to cause serious harm.

If the case involves severe injuries or possible UM/UIM issues, that evidence can matter even more. Our post on motorcycle UM/UIM claims when injuries are severe explains why the evidence package often drives the coverage and valuation fight.

7) What documentation usually helps most

Good claim documentation is often boring, but it wins more arguments than outrage does.

Helpful proof often includes:

- Photos of the bike and gear before the crash if you have them.

- Photos of every damaged item after the crash before cleaning, disposal, or repair.

- Receipts or invoices for helmets, jackets, boots, luggage, electronics mounts, and aftermarket parts.

- Install records or service invoices showing when accessories were added.

- Model names, sizes, and serial information where available.

- A written itemized list separating the bike, attached accessories, and separate personal property.

- Storage and tow records if the bike is in a yard where property could disappear.

If you do not have receipts for everything, do not assume the issue is over. Photos, old listings, service records, and account history may still help.

8) Common insurer pushback in these cases

Riders should expect some version of the following arguments.

“That’s just personal property. It isn’t covered.”

Sometimes that is partly right under a particular first-party policy. Sometimes it is overbroad. The right response is usually: identify the item, identify the coverage bucket, and ask the adjuster to point to the exact policy basis for the position.

“Your custom parts did not add that much value.”

That may be a real valuation dispute. Raw purchase price is not always the same as pre-loss value. But the insurer should still have to evaluate documented equipment accurately.

“You have no proof you owned that gear.”

This is why fast documentation matters. A rider who preserves the damaged items and compiles receipts, photos, and account records is in a much better position than a rider who throws everything away first.

“The bike payment includes everything.”

Sometimes that is true for certain attached equipment. Sometimes it is not. The rider should not assume the total-loss number automatically addressed the helmet, jacket, electronics, luggage, and every accessory dispute.

9) Practical steps after a totaled-motorcycle crash

If you are physically able after the collision:

- Photograph the motorcycle and every damaged gear item before repair or disposal.

- Keep the helmet, jacket, gloves, boots, and damaged accessories in a dry, secure place.

- Ask for the insurer’s valuation or appraisal report if the bike is declared a total loss.

- Create an itemized list separating the bike, attached aftermarket parts, and separate property.

- Gather receipts, card statements, shipping emails, install invoices, and pre-crash photos.

- Do not cash anything marked as a full and final settlement if you still dispute value.

- Keep towing, storage, and rental / loss-of-use paperwork together.

- Preserve the gear as injury evidence, not just reimbursement evidence.

If the crash also involved disputed roadway conditions rather than just another driver, our related post on motorcycle crashes caused by road hazards and public-body maintenance claims explains why the evidence timeline can become even more demanding.

Bottom line

If your motorcycle was totaled and your gear was destroyed in an Oregon crash, those losses may be recoverable.

But riders usually do better when they treat the claim as three separate proof problems:

- the motorcycle’s pre-loss value,

- the value of attached aftermarket parts or accessories,

- the value of separate damaged gear and property.

And just as important: do not treat the helmet, jacket, and damaged parts like disposable clutter. In a serious motorcycle case, they may help prove both the property loss and the injury story.

FAQ

Can I recover a damaged helmet and jacket after a motorcycle crash?

Often, yes, but the route depends on who is paying and what proof you have. The safest move is to preserve the items, photograph them, and document purchase or replacement information.

Does the totaled-bike payment automatically include aftermarket parts?

Not always. Some parts may be included in the bike valuation, some may be subject to separate accessory limits, and some disputes turn on whether the part actually added documented pre-loss value.

What if I do not have receipts for all my riding gear?

Receipts are best, but they are not the only proof. Pre-crash photos, service records, online account history, card statements, and photos of the damaged items may still help.

Should I throw away my damaged helmet after the crash?

Usually not right away. It may matter both as reimbursement evidence and as proof of impact or injury mechanism.

What if I disagree with the insurer’s total-loss value?

Ask for the valuation or appraisal report and review it closely. Oregon law also provides a process for payment of undisputed total-loss amounts while the valuation dispute continues.

Sources

Client-First Fee Promise

Client First = Bills First, Fees Second

Your unpaid medical bills do not have to make your lawyer's fee bigger. Johnson Law subtracts qualifying medical bills before calculating our fee, helping clients keep more of their settlement.

Applies to qualifying cases. Results vary.